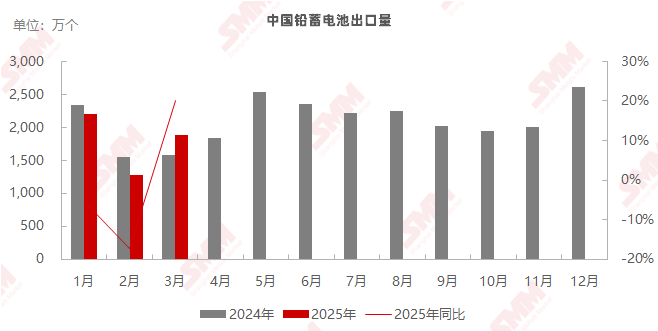

SMM April 22 News: According to customs data, lead-acid battery imports in March 2025 were 475,300 units, down 6.96% MoM and 9.63% YoY. Cumulative lead-acid battery imports from January to March 2025 were 1.3806 million units, up 2.03% YoY. Lead-acid battery exports in March 2025 were 18.894 million units, up 47.65% MoM and 20.08% YoY. Cumulative lead-acid battery exports from January to March 2025 were 53.7468 million units, down 1.45% YoY.

It is understood that the impact of the Chinese New Year on the domestic market was completely lifted in March, and overseas market demand gradually rebounded, including positive lead-acid battery orders from the automotive and ESS sectors. However, the SHFE/LME price ratio was unfavorable for battery exports. To seize or maintain overseas market share, most lead-acid battery exporters frequently took orders below domestic lead costs, resulting in MoM increases of 76.11% and 36.85% in starter battery and other lead-acid battery exports, respectively, in March.

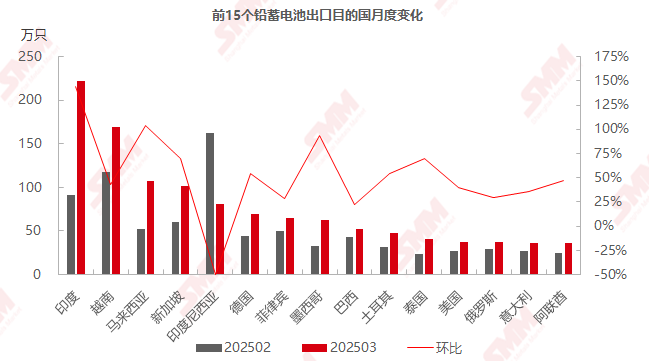

Since the beginning of this year, the US has escalated tariff hikes on China. As the US-China trade tariff war continues to intensify, the automotive industry has become one of the key areas impacted. As a major automotive component, lead-acid batteries have also been affected. Starter lead-acid battery imports in March 2025 fell 36.36% MoM. In Q1 2025, cumulative lead-acid battery exports were lower than the same period in 2024 (the SHFE/LME price ratio in Q1 2024 favored exports), with the share of exports to the US dropping to 0.21%.

》View more SMM lead industry chain database

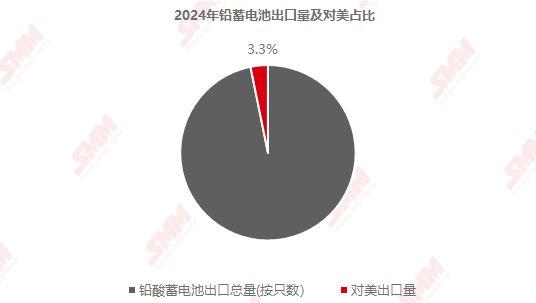

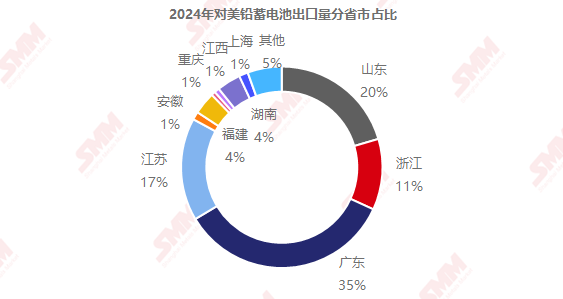

On April 2, 2025, US President Trump announced a 25% tariff hike on imported cars, with subsequent increases to 34%, 50%, 84%, 125%, 145%, and even up to 245%. In response, China imposed a 125% tariff on all US-origin imports. Faced with high tariffs, several major US automakers such as Ford and General Motors announced adjustments to their business strategies in China, suspending exports of certain car models to the Chinese market. This decision will further drag down lead-acid battery import and export business. According to overseas data, China's lead-acid battery imports from the US in 2024 were 70,900 units, accounting for 1.26% of total imports. Exports of lead-acid batteries to the US were 8.2979 million units, representing 3.3% of total exports, with the top three exporting provinces being Guangdong, Shandong, and Jiangsu.